If you’re a cat parent, you already know how quickly vet bills can stack up. A sudden illness, an unexpected accident, or even routine care can cost hundreds, sometimes thousands, of dollars. That’s where cat insurance comes in. But here’s the catch: not all coverage is the same. What you think is included may not be, and waiting until your cat is sick could leave you without the protection you need.

At PetCoverage.ai, we’ve seen too many families caught off guard by gaps in their policies. This guide breaks down exactly what does cat insurance cover in 2025, and what it doesn’t, so you can make the right choice for your furry friend today.

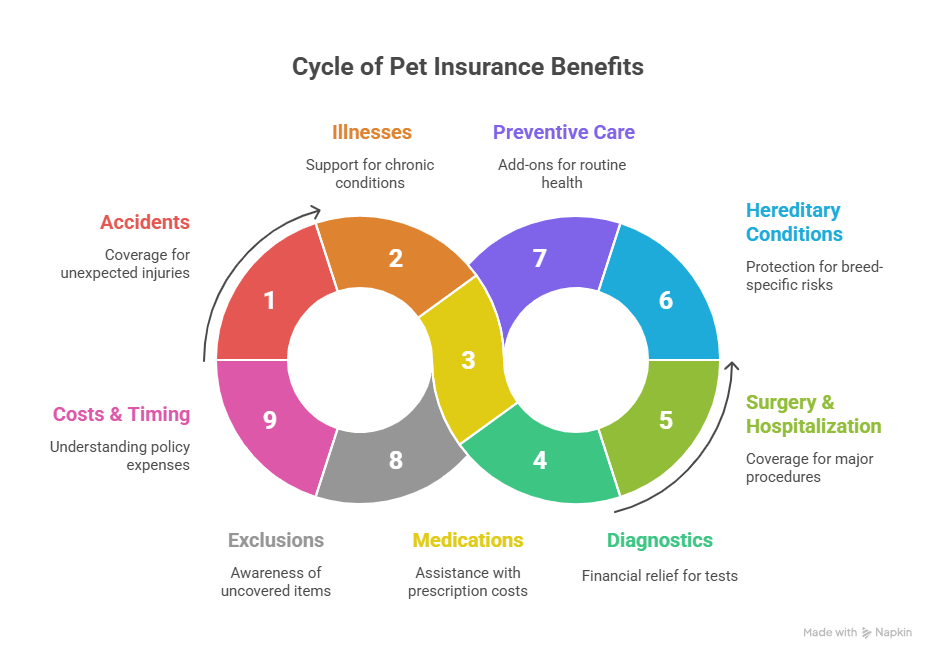

1. Accident Coverage: The Foundation of Every Policy

The most basic cat insurance plan covers accidents. This means if your cat swallows string, breaks a bone, or gets hit by a car, your insurance can step in to help with the vet bill. Treatments like X-rays, surgery, and hospitalization are usually included.

Why it matters: even indoor cats face risks. A fall from a shelf or a swallowed toy can quickly lead to a $2,000+ vet visit. Accident coverage ensures you won’t have to choose between your savings and your cat’s care.

Did you know? As of 2024, there are ~ 6.4 million insured pets in the U.S., with cat insurance growing 23.5% year-over-year.

2. Illness Coverage: The Real Lifesaver

Beyond accidents, illness coverage is where insurance really proves its value. It covers conditions like diabetes, kidney disease, and infections. These are common in cats, especially seniors, and can mean ongoing costs for medication, bloodwork, and check-ups.

Without coverage, chronic illnesses can cost pet parents thousands per year. With the right plan, most of these costs are reimbursed. In 2025, most comprehensive policies include illness protection, making it a must-have for peace of mind. If you’re asking what is pet insurance really for, illness coverage is one of its most important benefits.

3. Prescription Medications and Treatments

Modern veterinary medicine offers advanced treatments once reserved for humans. Think chemotherapy, insulin, or even allergy shots. Luckily, many cat insurance plans cover prescription medications.

But here’s the catch: not all do. Some providers limit drug coverage to accident-related prescriptions only. Before enrolling, check whether your plan covers long-term medications, especially if you’re insuring an older cat.

4. Lab Tests, Imaging, and Diagnostics

Cats are masters at hiding pain. That’s why vets often need blood tests, ultrasounds, or MRIs to uncover what’s really going on. These diagnostic tools are life-saving, but expensive.

The good news? Most 2025 insurance plans cover diagnostics if they’re medically necessary. Whether it’s routine bloodwork before surgery or advanced imaging to diagnose cancer, coverage here means answers without financial stress.

5. Hospitalization and Surgery

If your cat needs surgery or an overnight stay, costs can skyrocket. A simple abdominal surgery can exceed $3,000, and intensive care units may add another $1,000 a day.

This is where insurance steps in as a true safety net. In most cases, surgery, anesthesia, and hospitalization are covered, minus your deductible and co-pay. For cat owners, this can be the difference between treatment and heartbreak.

6. Hereditary and Congenital Conditions

Certain breeds, like Persians or Maine Coons, are prone to hereditary conditions. These can include heart disease, hip dysplasia, or respiratory issues. Years ago, many insurers excluded them, but in 2025, more providers are recognizing their importance.

Not every plan includes hereditary coverage, but the best ones do. If your cat is purebred, this type of protection isn’t optional, it’s essential.

7. Preventive Care: Often Optional but Valuable

Here’s where things get tricky. Wellness care, like vaccines, flea prevention, or dental cleanings, is usually not included in standard insurance. Instead, insurers offer optional wellness add-ons for an extra fee.

While not strictly “insurance,” these add-ons can save you money on expected annual care. And since preventive care keeps cats healthier longer, many pet parents find them worth it.

8. Exclusions: The Fine Print You Can’t Ignore

Here’s the warning every cat owner needs to hear: not everything is covered. Pre-existing conditions are almost always excluded, meaning if your cat already has diabetes before you buy a policy, future costs won’t be reimbursed.

Other exclusions may include:

Breeding or pregnancy-related care

Cosmetic procedures (declawing, ear cropping)

Experimental treatments

The takeaway: always read the fine print. Too many cat parents realize too late that their plan doesn’t cover what they thought it would.

9. The Real Costs and Why Timing Matters

So, how much is pet insurance in 2025? On average, accident-only plans cost around $10–$20/month, while comprehensive coverage with illness and wellness add-ons can range $30–$60/month.

But here’s the key: the earlier you enroll, the better. Younger, healthier cats lock in lower premiums and face fewer exclusions. Waiting until your cat is older, or already sick, can mean higher costs or outright denial. If you’re wondering when to get pet insurance, the answer is always as early as possible.

At PetCoverage.ai, we help you compare policies side by side so you can see exactly what’s covered and what it costs, before you commit.

Case Study: How Cat Insurance Saved Whiskers’ Life

In 2024, a family in California insured their 3-year-old rescue cat, Whiskers, with a comprehensive plan. Just six months later, Whiskers developed urinary blockages, requiring emergency surgery. The total bill? $4,800.

Because they had insurance, the family paid just $500 out of pocket. Without coverage, they admitted they may have delayed treatment, risking Whiskers’ life.

This is why timing and choosing the right plan matter. Tools like PetCoverage.ai help cat parents avoid surprises and secure the right protection before it’s too late.

Frequently Asked Questions (FAQs)

1. Does cat insurance cover dental care?

Standard policies cover dental if it’s related to an accident or illness (like an infected tooth). Preventive cleanings usually require a wellness add-on.

2. Can I get insurance for an older cat?

Yes, but it may cost more and exclude pre-existing conditions. Enrolling early means better rates and fewer restrictions.

3. What’s the difference between pet insurance and a savings account?

Insurance protects you from unpredictable, high-cost emergencies. A savings account may not be enough if bills exceed what you’ve set aside.

4. Is routine spaying or neutering covered?

Not usually. These are considered elective procedures, but some wellness add-ons may cover part of the cost.

5. When should I get pet insurance?

The best time is when your cat is young and healthy. That way, you lock in lower premiums and avoid pre-existing condition exclusions.

Key Takeaways

Cats hide pain until it’s serious, which means when you finally end up at the vet, the bill is rarely small. The biggest mistake cat parents make is assuming coverage will be there when it isn’t.

Focus on coverage that matters: Illnesses, hereditary conditions, and emergency surgeries should be non-negotiable in your plan.

Don’t get fooled by “cheap”: Policies with low premiums often cut out the very things cats need most, like chronic condition care or diagnostics.

Act before problems start: Enrolling your cat young ensures you avoid pre-existing condition exclusions and keeps your monthly costs manageable.

We broke down what does cat insurance cover in 2025, the fine print to watch for, and how to keep vet bills from draining your savings. Share this with another cat parent who’s on the fence, they’ll thank you later.

Stay connected with PetCoverage.ai: For real coverage breakdowns, side-by-side comparisons, and pet parent tips, follow us on Facebook, Instagram, TikTok, and LinkedIn.