Your dog yelps. The vet’s face turns serious. “We need to act now.” In that moment, your chest tightens, not because you don’t love your dog, but because you’re already seeing numbers. $1,800… $4,000… $7,000. That split-second fear, can we afford to say yes?, is exactly why pet health insurance for dogs matters.

At PetCoverage.ai, we don’t want money to be the reason a dog doesn’t get care. We built a free Policy Review that translates fine print into plain English, flags hidden gaps (like exam-fee exclusions), and shows if your plan will protect you on your worst day, not just your best.

Because the real question isn’t only “is pet insurance worth it?” It’s “will my plan work when my dog needs me most?”

What Drives the Cost of Pet Health Insurance for Dogs?

Pet insurance pricing has many moving parts, but they boil down to age, breed, location, plan type, and the “three money levers” (deductible, reimbursement %, annual limit). Together, these decide what you’ll pay month-to-month and how much help you’ll actually get when the bill is thousands.

Industry research confirms this, Bankrate’s 2025 review of how pet insurance premiums are determined found that age, breed, and zip code are consistently the strongest cost drivers, since they directly reflect a dog’s health risks and the emergency vet costs typical in that region. Here are the top reasons that drives the cost of pet health insurance for dogs;

Age: Puppies are cheaper, seniors cost more. Delay too long, and anything that starts before enrollment is “pre-existing” (not covered).

Breed: A Frenchie with airway issues, a Lab with hip risks, or a Golden with cancer tendencies will always cost more to insure than a mixed-breed.

Location: That same ACL surgery can cost $2,000 in a small town or $6,000 in a metro ER, your premium reflects where you live.

Plan type: Accident-Only is bare-bones; Accident & Illness is the safety net most people need; Wellness add-ons only cover routine care.

Money levers: Adjusting deductible, reimbursement %, and annual limit changes both your monthly premium and your out-of-pocket hit at claim time.

Brand warning: The cheapest plan often looks good until an emergency. Cancer sub-limits, exam fee exclusions, and long waiting periods can leave you exposed when you need coverage most.

Action tip:

For high-risk breeds or big-city care: aim for $250–$500 deductible, 90% reimbursement, and $10k+ annual limit (ideally unlimited).

For budget-conscious owners: trim wellness add-ons first, but never drop below 80% reimbursement.

Not sure how to balance those levers? Upload your policy to PetCoverage.ai for a free gap check, we’ll stress-test it against real-world emergencies so you know exactly where you stand before the next vet bill.

Plan Type Changes Everything: Accident-Only vs. Accident & Illness vs. Wellness

1. Accident-Only is the entry-level safety net. It helps when life gets weird: swallowed socks, broken bones, cuts, toxic ingestions. It’s cheaper each month, but it does not cover illnesses like diabetes, cancer, or skin infections.

2. Accident & Illness is the workhorse plan most families choose. It typically covers ER care, hospital stays, diagnostics (x-rays, bloodwork, ultrasound, CT/MRI), meds, and treatments for common illnesses. This is the plan that helps when your vet says, “We need to act now.”

3. Wellness add-ons help with the expected stuff: annual exams, vaccines, routine dental cleanings, parasite prevention. They don’t save you from big ER bills, but they can make predictable costs more manageable.

4. Bottom line: If you can only afford one thing, choose Accident & Illness. Then add wellness if it pays for things you already buy each year.

Start a new quote with the right base plan, or upload your policy for a wellness math check.

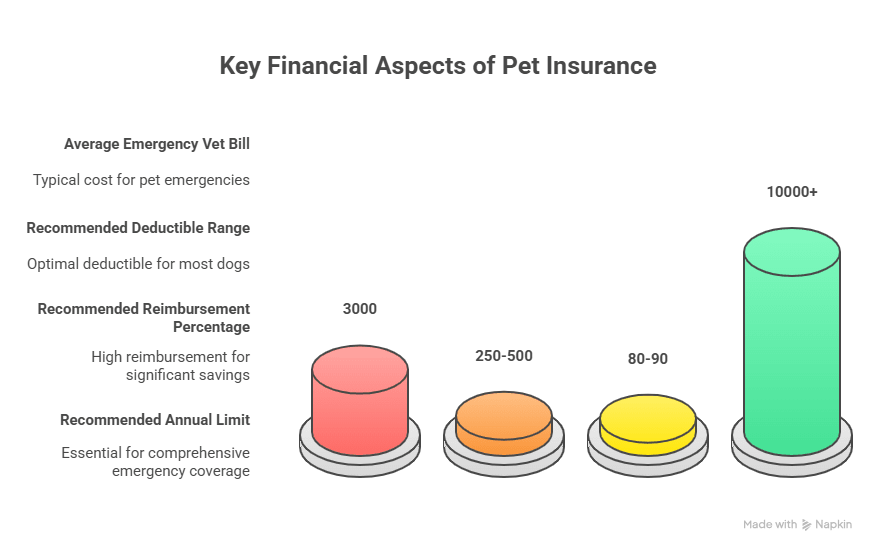

The Three Money Levers That Decide Your Real Out-of-Pocket Cost

These three settings shape what you pay when crisis hits:

Deductible (what you pay first): Common options are $200–$1,000. Lower deductible = higher monthly premium but smaller shock at checkout. For most families, $250–$500 is a sweet spot.

Reimbursement % (what the insurer pays after deductible): 70%, 80%, or 90% are common. The higher this is, the less you pay on big bills. We like 80–90% if emergencies worry you.

Annual limit (max the plan pays in a year): Ranges from $5,000 to unlimited. If specialty care is common in your area, or your dog is a high-risk breed, aim for $10,000+ (or unlimited).

Example: $3,000 ER bill • $250 deductible • 80% reimbursement

Insurer pays ≈ $2,200

You pay ≈ $800 (including the deductible)

Set these wrong, and you’ll still face big bills. Set them right, and you can say yes to care faster.

Claims, Reimbursements, and the Part Nobody Tells You About

Here’s what how to get pet insurance looks like in real life after you enroll:

Go anywhere: Most plans let you use any licensed vet, ER, or specialist, no network drama.

Pay first, claim second: You pay the clinic, then upload your invoice and medical notes in your insurer’s app/portal.

Reimbursement timing: Many carriers pay within 5–10 business days. Some offer direct pay to the clinic for big ER bills, which can reduce the deposit you owe at check-in.

Keep records: Save invoices, itemized receipts, and any lab reports. Fast, clean claims get paid faster.

Pro tip: Choose a plan that covers exam fees. Otherwise, expect $75–$250 per visit out-of-pocket, even in the ER.

Brand urgency: Claim stress is real during emergencies. Build an emergency file now: insurer app login, vet’s number, your policy PDF, and a photo of your dog’s meds list.

Need a pre-check? Upload your policy for a claims-readiness review.

The Fine Print That Quietly Raises Your Cost (Even If the Premium Looks Low)

Warning: Don’t Skip This Part

Here’s where “good-looking” plans go sideways:

Exam-fee exclusions: You still pay the visit fee each time (often $75–$250), even if the treatment is covered.

Bilateral clauses: If one knee or eye has a pre-existing issue, the mirror side may be excluded later.

Sub-limits inside big limits: “$10,000 annual limit”… but only $2,500 for cancer or $1,000 for dental.

Lengthy waiting periods: Anything that happens during the wait can be tagged “pre-existing.”

Dental exclusions: Cleanings and extractions are often excluded unless you add wellness (and even then, caps may apply).

These don’t just change coverage, they change your real cost when it matters.

Real Costs, Real Life: A Short Case Study

Cassie, a 5-year-old mixed breed, had three separate issues in one year: an ear infection (~$200), pancreatitis (~$900), and a tooth abscess (~$2,500). With a $500 deductible, 70% reimbursement, $2,500 annual limit, Mickey’s family paid about $1,706 total. With a $250 deductible, 80% reimbursement, $5,000 annual limit, they paid about $1,472 total. Without insurance, they would’ve paid ~$3,600 out of pocket.

What it proves: The right levers matter. Higher reimbursement and higher limits reduce pain in a “bad” year.

How Much Does Pet Health Insurance for Dogs Cost Each Month?

Short answer: it depends on your dog, your zip code, and your settings. We’ve seen:

Accident-Only: very low monthly cost, but limited protection

Accident & Illness: the true “safety net,” typically moderate monthly cost

Wellness add-ons: small extra each month for predictable routine care

Smart setup for most families:

Accident & Illness base plan

$250–$500 deductible

80–90% reimbursement

$10,000+ annual limit

Add wellness only if it covers what you already buy (and the math pencils out)

Want personalized pricing? Try our calculator or send your quote, we’ll break it down line by line.

Frequently Asked Questions (FAQs)

1. Will insurance cover my dog’s current issue?

Probably not. If symptoms or diagnosis started before enrollment or during the waiting period, it’s usually marked “pre-existing.” New problems after the wait are typically eligible.

2. Can I use any vet or ER?

Yes, most pet insurers let you visit any licensed vet, specialist, or ER. You pay the bill, then submit a claim for reimbursement.

3. What’s a good annual limit?

Aim for $10,000+. Specialty care adds up fast, and low caps create surprise out-of-pocket costs.

4. How fast do claims get paid?

Many pay within 5–10 business days. Some carriers now offer direct pay to clinics for large ER bills.

5. My premium went up, why?

Aging pets, rising vet costs, and regional trends can all push premiums higher. We can help you adjust levers to keep coverage strong without breaking your budget.

Key Takeaways

When minutes matter, you shouldn’t be doing math. Your dog, your location shape the cost of pet health insurance for dogs, and your plan settings, but the biggest cost of all is being unprepared when the ER doctor says, “We need to act now.” This is when emergency vet costs can skyrocket.

Set the right levers. A smart deductible, 80–90% reimbursement, and $10,000+ limit protect you from the big stuff.

Read past the premium. Watch for exam-fee exclusions, sub-limits, bilateral rules, and waiting periods that quietly raise your real cost.

Act early. Enroll your dog while it is healthy and revisit your plan annually as needs change.

We covered what drives price, how claims work, what’s covered (and not), and where families get surprised. Keep the conversation going, drop questions in the comments and tell us what you want us to decode next.

Stay connected with PetCoverage.ai: For practical tips, claim-time checklists, and transparent breakdowns, follow us on Facebook, Instagram, TikTok, and LinkedIn. We share real stories, real math, and ways to protect both your pet and your peace of mind.