It’s a sunny afternoon. Your cat is curled up in the window, or your dog is chasing a ball at the park. Then, in seconds, everything shifts, a fall, a seizure, a sudden collapse. You’re at the emergency vet, the doctor’s face is serious, and you’re handed a $7,500 estimate for life-saving treatment.

In that moment, will you have the financial safety net your pet deserves? Or will you have to make an impossible choice and wonder “should I have pet insurance” sooner?

This isn’t rare. Veterinary costs have skyrocketed, emergency surgeries now average $4,000–$12,000. In 2025, pet insurance is no longer “nice to have”, it’s the only way to protect both your heart and your wallet.

Why Waiting Could Be a Dangerous Mistake

Too many pet parents think, “I’ll get insurance when I need it.” Here’s the truth:

Pre-existing conditions aren’t covered. Wait until your pet is sick, and no insurer will pay for it.

Waiting periods delay coverage. Illnesses, accidents, even surgeries may not be covered for weeks or months after signing up.

Cheap plans can leave you uncovered when it matters most. That $15/month plan might skip cancer treatment, hip surgeries, or even emergency hospital stays.

In North America, pet insurance premiums surged from $4.2B in 2023 to $5.2B in 2024, a 20.8% year-over-year increase. The industry also insured a record 7.03 million pets, showing just how fast adoption is growing. Yet despite this momentum, many pet parents still wait too long to enroll, only to discover gaps in coverage when emergencies strike.

Warning: Waiting could cost you more than money, it could cost your pet’s life. Sign up when they’re healthy so coverage is ready when you need it. If you’re asking yourself, “should I have pet insurance now or later?”, or even wondering “is there life insurance for dogs”, the best step is to act before it’s too late.

What Is Pet Insurance and Why Does It Matter Now?

Pet insurance is like a financial safety net for vet care. You pay a monthly premium, and when your pet gets sick or injured, the insurer reimburses a big part of your bill.

Why does it matter so much in 2025?

Vet bills are higher than ever. Emergency visits average $1,500–$5,000. Advanced care like MRIs or chemo can exceed $10,000.

Pets are living longer. More years means more chances of chronic conditions like diabetes or arthritis.

Better treatments exist, but they come at a cost. Life-saving procedures are available, but without coverage, many families can’t afford them.

At PetCoverage.ai, we’ve built a free policy review tool to help pet parents ensure their coverage matches today’s realities, not yesterday’s prices. If you’ve ever asked yourself “should I have pet insurance before my pet gets older?” the answer is yes, timing matters.

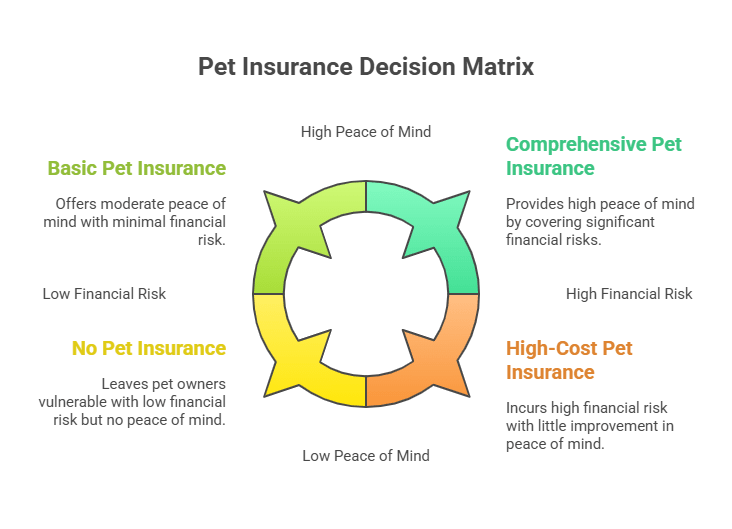

How to Choose the Right Pet Insurance (and Avoid Common Traps)

Choosing a plan isn’t about picking the cheapest monthly fee, it’s about making sure you’re truly covered.

Look beyond the monthly premium. Low cost often means low protection. Consider deductibles, reimbursement rates, and annual limits.

Check for breed-specific exclusions. Some policies won’t cover conditions common in your pet’s breed.

Understand waiting periods. Know how long until accident, illness, and orthopedic coverage starts.

Review coverage limits. Annual and lifetime caps can leave you with massive bills after one major incident.

Consider age factors. Senior pets face higher costs and sometimes exclusions, don’t wait until coverage is limited.

We’ve helped thousands of pet parents review their policies and switch to plans that truly protect them. One client, Mark, had a “budget” policy for his Golden Retriever, Daisy. When she was diagnosed with cancer, he discovered chemo wasn’t included. We guided him to comprehensive coverage for his next pet, and now he pays less than before while being fully protected.

Case Study: How Insurance Saved Bella the Beagle

Last year, one of our clients, Neneth, called us in tears. Her Shih tzu, Princess, needed emergency surgery for a swallowed toy. The bill? $6,800 upfront. Luckily, Neneth had recently upgraded her plan with our help, her policy covered 90% of the cost, and Neneth was back home within days.

Real-Life Proof: Having the right coverage doesn’t just save money, it saves lives. And this is what we do every day at PetCoverage.ai: ensure pets get the care they need, without hesitation. Next time you ask yourself “should I have pet insurance before emergencies happen?” remember Bella’s story.

What Pet Insurance Covers (and What It Doesn’t in 2025)

Covers:

Accidents: broken bones, swallowed objects, toxic ingestion

Illnesses: cancer, diabetes, infections, allergies, chronic conditions

Optional wellness add-ons: exams, vaccines, parasite prevention

Doesn’t Cover:

Pre-existing conditions

Elective procedures (declawing, ear cropping)

Breeding, pregnancy, grooming

2025 Tip: Vet bills are climbing faster than ever, and policies change yearly. Always read the fine print. Coverage varies widely, and we’ve seen “comprehensive” policies that quietly exclude the most common needs. This is another reason why asking “should I have pet insurance right now?” is critical.

Frequently Asked Questions (FAQs)

1. Should I have pet insurance if my pet is healthy?

Yes. Signing up early locks in coverage before any condition becomes “pre-existing,” ensuring future care is covered.

2. Is pet insurance worth it if I have savings?

Even a strong savings account can vanish with one major emergency. Insurance protects against catastrophic costs while preserving your savings.

3. Should I get pet insurance for my cat?

Absolutely. Cats often hide illness until it’s severe, making early detection and treatment crucial, and costly without coverage.

4. Can you have two pet insurance policies?

Technically yes, but most insurers coordinate benefits. One solid plan is usually enough.

5. Can you cancel pet insurance at any time?

Yes, but you’ll lose coverage immediately, and pre-existing conditions won’t be covered if you reapply later.

Key Takeaways

Pet insurance isn’t just about saving money, it’s about saving lives. If there’s one thing to remember, it’s this: waiting costs more than acting now.

Secure Coverage While They’re Healthy: Enroll early to avoid denied claims for pre-existing conditions.

Understand Your Policy Inside and Out: Know what’s covered, and what’s not, before you face a crisis.

Protect What Matters Most: The right plan is peace of mind for you and a lifeline for your pet. Start with our free policy review today.

We’ve shown why acting early saves thousands, what pet insurance really costs, and how to avoid common mistakes pet parents make.

For ongoing tips, guides, and real-life stories on protecting your pet’s health, follow Facebook, Instagram, TikTok, and LinkedIn.