Chinchin, a playful half-Pomeranian, racked up thousands in vet bills after a year filled with unexpected accidents and illnesses. Her owner quickly learned that the deductible she chose made all the difference, turning what could have been financial chaos into manageable costs.

Stories like this are why pet insurance has become more than just a financial backup, it’s now a critical part of responsible pet ownership in 2025. With veterinary care costs climbing every year, pet parents are asking the right questions: what is an annual deductible for pet insurance, how much should I choose, and how does it affect my overall costs?

This guide explains everything you need to know about annual deductibles in pet insurance, how they impact real-life expenses, and how to choose the right plan for your pet’s needs.

Don’t Pick the Wrong Deductible

Don’t let the wrong deductible cost you thousands. An annual deductible is the amount you must pay out of pocket each year before your pet insurance starts covering veterinary bills, and choosing the wrong one is a costly mistake many pet parents regret.

For anyone asking “how does pet insurance work?” the deductible is the key. It’s your share of responsibility before coverage kicks in, and it can make or break your budget during emergencies.

Here’s how it works in practice:

Fixed yearly amount: If your deductible is $500, you’ll need to pay that amount in vet costs first. After you’ve met that number, your insurance will begin reimbursing eligible expenses.

Reimbursement starts after deductible: Once the deductible is met, your provider pays according to your chosen reimbursement rate (for example, 70%, 80%, or 90%).

Annual reset: Deductibles reset at the start of each policy year, meaning you start fresh each year, regardless of how much you spent the previous year.

Avoid this costly mistake: guessing your deductible. Use PetCoverage.ai’s calculator to see exactly how much you’d be paying in real scenarios before you commit.

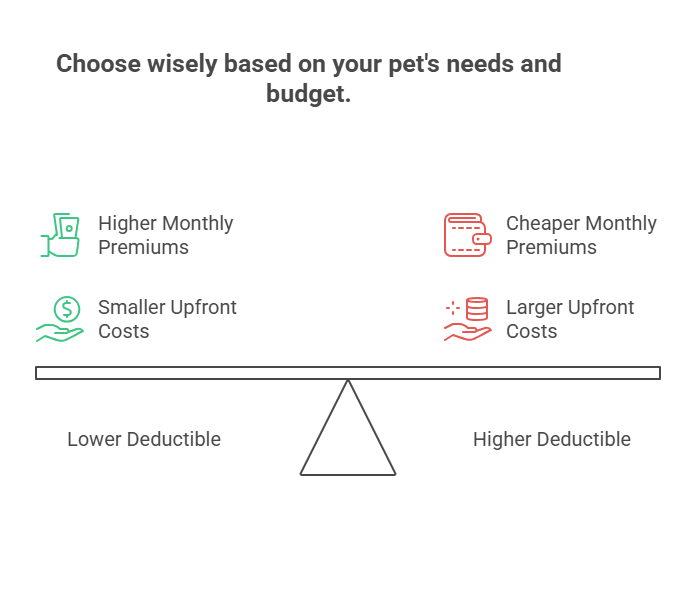

Why It Matters

The deductible you choose directly impacts your monthly premium and the amount you’ll pay for unexpected veterinary visits.

Lower deductible → Higher monthly premiums but less out-of-pocket when accidents or illnesses occur.

Higher deductible → Lower monthly premiums but more upfront costs if your pet needs care.

Don’t guess. Use PetCoverage.ai’s deductible calculator to see exactly how different choices affect your costs.

Example: Breaking It Down (With Calculator)

Using PetCoverage.ai’s calculator, let’s look at a real-life example to understand how does pet insurance work when deductibles are involved:

Vet bill: $1,000

Deductible: $500

Reimbursement rate: 80%

Here’s how the math plays out:

You first cover the $500 deductible.

The remaining $500 is eligible for coverage.

With 80% reimbursement, the insurance pays $400.

You pay the remaining 20% ($100).

Your total out-of-pocket cost: $600 ($500 deductible + $100 coinsurance).

Insurance contribution: $400.

This example illustrates why deductibles are more than just a line in your policy, they’re a crucial part of financial planning for pet care. The right deductible can mean the difference between manageable bills and overwhelming costs when your pet needs care.

Don’t leave it to guesswork. Use PetCoverage.ai’s calculator to model your pet’s real-life scenarios, see exactly how your deductible choice affects your costs, and avoid a surprise bill.

For pet parents asking, “is pet insurance worth it?” the answer often depends on the deductible. That’s why PetCoverage.ai tools let you run side-by-side comparisons and get personalized recommendations based on your pet’s age, breed, and health history.

With the right insights, you can make a confident choice today, before a vet emergency makes the wrong deductible a very expensive mistake.

Warning: Common Deductible Mistakes to Avoid

Many pet parents unknowingly choose deductibles that set them up for disaster. Here are the red flags:

Picking the highest deductible just to lower monthly premiums, only to face a $1,500 bill before coverage begins.

Forgetting deductibles reset every year. One bad year can wipe out your savings.

Ignoring breed and age risks, senior pets or breeds prone to conditions often benefit from lower deductibles.

Don’t fall into these traps. Use PetCoverage.ai tools and personalized recommendations to avoid a costly mistake.

Choosing the Right Deductible for Your Pet

When deciding between a $250, $500, or $1,000 deductible, here are the key factors to weigh:

Pet’s Age & Breed – Senior pets or breeds prone to hereditary conditions may benefit from lower deductibles since claims are likely.

Your Budget – If you want to keep monthly premiums low, a higher deductible may be a better option. If you’d rather avoid big surprise vet bills, a lower deductible works best.

Frequency of Vet Visits – Pets with chronic conditions or a history of accidents may hit their deductible quickly each year.

According to Forbes Advisor, pet insurance deductibles typically range from $50 to $1,000, with $250 being a common choice. Lower deductibles come with higher premiums, while higher deductibles reduce premiums but require larger upfront spending before coverage begins.

Case Study: Chinchin’s $7,000 Lesson

Take Chinchin, a playful half-Pomeranian, who had an especially unlucky year, including an ear infection, a swallowed toy, and a knee injury. Her owner, Amalia Talan, faced over $7,000 in vet bills.

With a $500 deductible, Chinchin’s insurance covered most of the expenses after the first $500 was met, leaving Amalia with manageable co-pays.

With a $1,500 deductible, Amalia would have had to shell out thousands before any coverage kicked in.

This proves why deductible choice is often more important than just premiums. For many pet parents, asking “is pet insurance worth it” really comes down to whether the deductible makes coverage affordable when it’s needed most.

How PetCoverage.ai Helps Pet Parents Decide

Finding the right deductible can be overwhelming. That’s where tools like PetCoverage.ai make it easy:

Policy Comparison: Quickly compare plans across providers

Deductible Calculator: See how your costs change under different scenarios

Personalized Plans: Tailored recommendations based on your pet’s breed, age, and health profile

Instead of guessing, pet parents can model real-life scenarios (like Chinchin’s case) and make confident choices.

Frequently Asked Questions (FAQs)

1. Do deductibles apply per condition or per year?

Most pet insurance plans use an annual deductible that resets each year. A few offer per-condition deductibles, which apply separately to each illness or injury.

2. Are wellness visits counted toward the deductible?

No. Wellness visits usually don’t count toward the deductible. Deductibles apply to accidents and illnesses unless wellness is bundled in your plan.

3. Can I change my deductible after enrolling?

Yes. You can usually adjust your deductible at renewal. Lowering it raises premiums, while raising it lowers premiums.

4. Is a higher deductible always better?

No. A higher deductible means lower monthly costs but higher upfront expenses during emergencies. It’s only better if you can afford larger out-of-pocket bills.

Key Takeaways

In wrapping up our look at what is an annual deductible for pet insurance in 2025, it’s clear that understanding how deductibles work is essential for making smarter financial and healthcare decisions for your pets. Here are three key takeaways:

Balance Cost & Coverage: Choosing the right deductible involves weighing monthly premium savings against potential out-of-pocket costs during emergencies.

Plan for the Unexpected: A clear understanding of how does pet insurance work with deductibles ensures you’re financially prepared for sudden veterinary expenses without sacrificing your pet’s care.

Customize for Your Pet: Factors like breed, age, and health status should guide deductible selection to ensure coverage truly fits your pet’s needs.

Don’t leave this to chance. Use our calculator to see how different deductible levels affect your actual costs, and get personalized recommendations tailored to your pet’s needs with PetCoverage.ai tools.

Make the smart choice now, before a single vet bill turns into a costly mistake.

For more tips on choosing the right pet insurance plan and managing costs, follow us on Facebook, Instagram, TikTok, and LinkedIn.